Focus on the BIG picture.

Sunday, May 10, 2026

Outside the box.

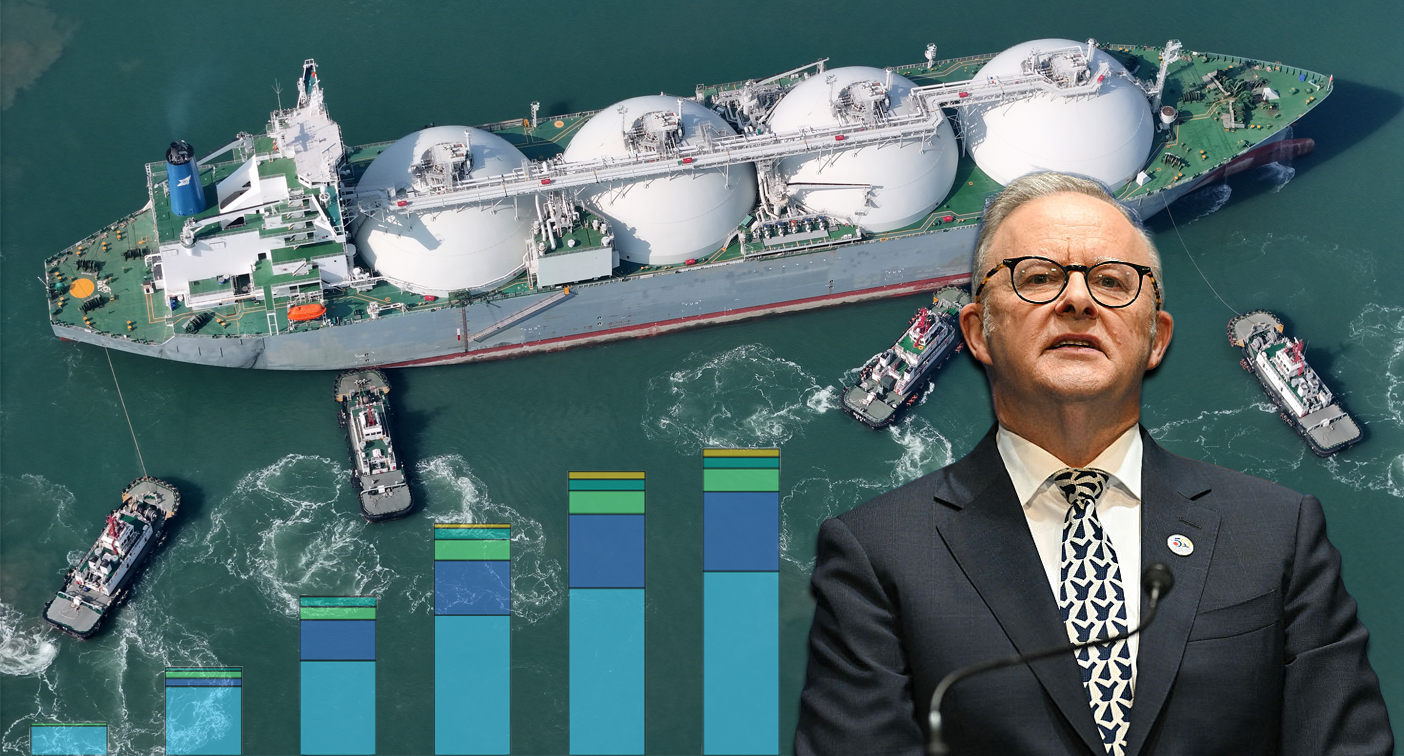

China’s Energy Pivot and America’s LNG Boom Are Squeezing Australia’s Gas Strategy

Beijing’s shift away from US liquefied natural gas is reshaping global energy flows, but the larger surge in American exports is intensifying pressure on Australia’s long-term position in Asian gas markets.

Global liquefied natural gas markets are being reshaped by a structural shift in trade flows as China reduces direct purchases of American LNG while the United States simultaneously expands export capacity at record speed, creating a more competitive environment that is challenging Australia’s long-standing role as Asia’s dominant gas supplier.

The central issue is not a single trade dispute or cargo diversion.

It is the emergence of a new energy market structure in which geopolitical friction, oversupply risks and changing Asian demand patterns are colliding at the same time.

Australia’s gas industry, which spent more than a decade building massive export projects aimed primarily at Asian buyers, now faces pressure from both sides: weakening Chinese demand growth and aggressive expansion by US exporters.

China’s move away from direct US LNG imports accelerated after tariff escalation between Washington and Beijing earlier this year.

Beijing imposed retaliatory tariffs on American LNG as part of the broader trade conflict triggered by the Trump administration’s tariff measures.

Chinese buyers responded by rerouting or swapping US cargoes into other markets rather than importing them directly.

What is confirmed is that Chinese imports of US LNG dropped sharply after the tariff measures took effect, and cargoes have increasingly been redirected toward Europe and other Asian buyers through trading intermediaries.

Chinese firms are also relying more heavily on domestic gas production, pipeline imports from Russia and Central Asia, and alternative LNG suppliers including Australia, Qatar, Indonesia and Brunei.

At first glance, that appears favorable for Australian exporters.

China remains one of Australia’s largest LNG customers, and reduced direct US-China trade theoretically opens market share opportunities.

But the larger market reality is more complicated and potentially more damaging for Australia over time.

The United States is continuing to expand LNG export capacity rapidly despite the trade conflict.

New terminals under construction along the Gulf Coast are increasing total American export capability to levels capable of reshaping global supply balances for years.

Even if Chinese buyers avoid direct purchases, US cargoes still enter the global system and compete indirectly with Australian exports in Europe and Asia.

That matters because LNG is increasingly a globally interconnected commodity rather than a rigid bilateral trade.

Cargoes can be swapped, rerouted and resold across regions depending on price movements and shipping economics.

A molecule originally destined for China can ultimately displace Australian supply elsewhere.

Australia’s challenge is rooted in geography, cost structures and timing.

Many Australian LNG projects were developed during the commodity boom of the early 2010s under assumptions of continuously rising Chinese gas demand and relatively constrained competition.

Those projects involved extremely high capital costs, complex offshore infrastructure and long-term pricing expectations that now look less secure.

American LNG exporters operate under a different model.

US projects benefit from abundant shale gas production, flexible destination clauses and increasingly large export infrastructure.

They also gained strategic momentum from Washington’s push to position American energy exports as a geopolitical tool after Russia’s invasion of Ukraine disrupted global gas markets.

The result is a global supply wave that is arriving just as China’s energy consumption outlook becomes more uncertain.

Chinese industrial growth is slowing compared with earlier decades, renewable energy deployment is accelerating and domestic gas production continues to rise.

China is still a massive energy importer, but the assumption that its LNG demand would expand endlessly is weakening.

Australia now faces another problem: domestic political backlash against its own gas export system.

High local energy prices have intensified criticism that Australian households and manufacturers are subsidizing exports while facing tightening domestic supply conditions.

Canberra has increasingly discussed intervention measures, reservation policies and export controls to stabilize local markets.

That creates tension between Australia’s role as a reliable global supplier and domestic political demands for cheaper energy.

Investors are watching closely because LNG projects require decades-long certainty.

Any perception of unstable policy settings can affect financing decisions for future developments.

The strategic stakes extend beyond economics.

LNG has become deeply tied to geopolitical influence across the Indo-Pacific.

Energy supply relationships shape diplomatic leverage, infrastructure investment and security partnerships.

Australia has long treated LNG exports as both a commercial engine and a strategic asset linking it to Japan, South Korea and China.

But the regional balance is shifting.

Qatar is expanding production aggressively.

The United States is becoming the dominant swing supplier in global LNG trade.

Southeast Asian producers are increasing output.

China is diversifying energy sources while investing heavily in renewables and nuclear generation.

The pressure on Australia is therefore structural rather than temporary.

Its export industry still benefits from proximity to Asian buyers and long-term contracts signed years ago.

Existing projects continue generating substantial revenue.

But future growth assumptions are becoming harder to defend.

The larger irony is that the US-China trade confrontation, initially expected to damage American LNG ambitions, may ultimately strengthen US influence over global gas markets.

Chinese buyers can avoid direct imports from America while still relying on a global market increasingly shaped by US supply volumes.

Australia’s energy strategy was built on the idea that Asian gas demand would remain strong enough to absorb expensive long-term export capacity with limited competitive pressure.

That assumption is now under sustained strain from China’s energy diversification, slower demand growth and the sheer scale of expanding American LNG exports.

What is confirmed is that global gas trade is entering a more fragmented and intensely competitive era, and Australia’s LNG sector is being forced to adapt from a position of relative dominance into one of strategic defense.

The central issue is not a single trade dispute or cargo diversion.

It is the emergence of a new energy market structure in which geopolitical friction, oversupply risks and changing Asian demand patterns are colliding at the same time.

Australia’s gas industry, which spent more than a decade building massive export projects aimed primarily at Asian buyers, now faces pressure from both sides: weakening Chinese demand growth and aggressive expansion by US exporters.

China’s move away from direct US LNG imports accelerated after tariff escalation between Washington and Beijing earlier this year.

Beijing imposed retaliatory tariffs on American LNG as part of the broader trade conflict triggered by the Trump administration’s tariff measures.

Chinese buyers responded by rerouting or swapping US cargoes into other markets rather than importing them directly.

What is confirmed is that Chinese imports of US LNG dropped sharply after the tariff measures took effect, and cargoes have increasingly been redirected toward Europe and other Asian buyers through trading intermediaries.

Chinese firms are also relying more heavily on domestic gas production, pipeline imports from Russia and Central Asia, and alternative LNG suppliers including Australia, Qatar, Indonesia and Brunei.

At first glance, that appears favorable for Australian exporters.

China remains one of Australia’s largest LNG customers, and reduced direct US-China trade theoretically opens market share opportunities.

But the larger market reality is more complicated and potentially more damaging for Australia over time.

The United States is continuing to expand LNG export capacity rapidly despite the trade conflict.

New terminals under construction along the Gulf Coast are increasing total American export capability to levels capable of reshaping global supply balances for years.

Even if Chinese buyers avoid direct purchases, US cargoes still enter the global system and compete indirectly with Australian exports in Europe and Asia.

That matters because LNG is increasingly a globally interconnected commodity rather than a rigid bilateral trade.

Cargoes can be swapped, rerouted and resold across regions depending on price movements and shipping economics.

A molecule originally destined for China can ultimately displace Australian supply elsewhere.

Australia’s challenge is rooted in geography, cost structures and timing.

Many Australian LNG projects were developed during the commodity boom of the early 2010s under assumptions of continuously rising Chinese gas demand and relatively constrained competition.

Those projects involved extremely high capital costs, complex offshore infrastructure and long-term pricing expectations that now look less secure.

American LNG exporters operate under a different model.

US projects benefit from abundant shale gas production, flexible destination clauses and increasingly large export infrastructure.

They also gained strategic momentum from Washington’s push to position American energy exports as a geopolitical tool after Russia’s invasion of Ukraine disrupted global gas markets.

The result is a global supply wave that is arriving just as China’s energy consumption outlook becomes more uncertain.

Chinese industrial growth is slowing compared with earlier decades, renewable energy deployment is accelerating and domestic gas production continues to rise.

China is still a massive energy importer, but the assumption that its LNG demand would expand endlessly is weakening.

Australia now faces another problem: domestic political backlash against its own gas export system.

High local energy prices have intensified criticism that Australian households and manufacturers are subsidizing exports while facing tightening domestic supply conditions.

Canberra has increasingly discussed intervention measures, reservation policies and export controls to stabilize local markets.

That creates tension between Australia’s role as a reliable global supplier and domestic political demands for cheaper energy.

Investors are watching closely because LNG projects require decades-long certainty.

Any perception of unstable policy settings can affect financing decisions for future developments.

The strategic stakes extend beyond economics.

LNG has become deeply tied to geopolitical influence across the Indo-Pacific.

Energy supply relationships shape diplomatic leverage, infrastructure investment and security partnerships.

Australia has long treated LNG exports as both a commercial engine and a strategic asset linking it to Japan, South Korea and China.

But the regional balance is shifting.

Qatar is expanding production aggressively.

The United States is becoming the dominant swing supplier in global LNG trade.

Southeast Asian producers are increasing output.

China is diversifying energy sources while investing heavily in renewables and nuclear generation.

The pressure on Australia is therefore structural rather than temporary.

Its export industry still benefits from proximity to Asian buyers and long-term contracts signed years ago.

Existing projects continue generating substantial revenue.

But future growth assumptions are becoming harder to defend.

The larger irony is that the US-China trade confrontation, initially expected to damage American LNG ambitions, may ultimately strengthen US influence over global gas markets.

Chinese buyers can avoid direct imports from America while still relying on a global market increasingly shaped by US supply volumes.

Australia’s energy strategy was built on the idea that Asian gas demand would remain strong enough to absorb expensive long-term export capacity with limited competitive pressure.

That assumption is now under sustained strain from China’s energy diversification, slower demand growth and the sheer scale of expanding American LNG exports.

What is confirmed is that global gas trade is entering a more fragmented and intensely competitive era, and Australia’s LNG sector is being forced to adapt from a position of relative dominance into one of strategic defense.