Focus on the BIG picture.

Tuesday, Dec 09, 2025

Outside the box.

Trump’s Interest in Australia’s Retirement Model Sparks Debate Over Its Fit for the United States

The former president’s praise for Australia’s compulsory savings system prompts questions about whether such a framework could be implemented in America

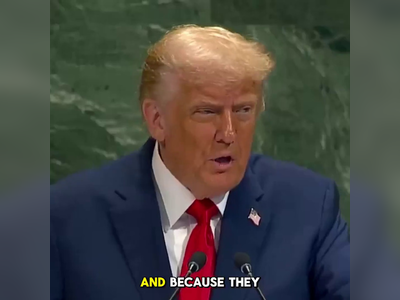

Donald Trump has signaled that he is examining Australia’s compulsory retirement savings model as a potential blueprint for reforming America’s fragmented retirement system.

His remarks, highlighting what he described as a highly successful approach, have ignited a discussion over whether a similarly mandated structure could realistically function within the United States.

Australia’s superannuation framework requires employers to contribute a fixed portion of each employee’s wages into a managed retirement fund.

This locked-in savings mechanism has built one of the world’s largest national investment pools and provides most Australian workers with a reliable foundation for retirement income.

Trump praised the model for its discipline, stability and long-term performance, noting that it has produced stronger retirement outcomes than many voluntary savings systems.

The United States, by contrast, relies on a patchwork of employer-provided plans, personal savings and future Social Security benefits.

Millions of Americans lack access to retirement accounts, and savings levels vary widely across income groups.

Administration officials have indicated that exploring an Australian-style model reflects concerns about demographic pressures, widening savings gaps and growing uncertainty over the future strength of Social Security.

Supporters of the idea argue that a compulsory contribution system could dramatically strengthen the financial security of working Americans.

They point to Australia’s experience as evidence that consistent contributions and professional fund management build far more reliable retirement outcomes than voluntary systems, which often leave lower-income or irregular-income workers behind.

But major obstacles remain.

A mandate requiring employers to contribute to every worker’s retirement fund would mark a substantial shift from established U.S. labour and tax norms.

Small businesses, gig-economy employers and industries with fluctuating workforce patterns may find such requirements burdensome.

Transitioning the nation to a system resembling superannuation would also involve complex political negotiations and long-term legislative restructuring.

Some economists warn that, without additional safeguards, an imported model could deepen disparities among workers whose earnings patterns differ significantly from the more stable employment structures common in Australia.

They note that any American adaptation would need careful provisions to protect part-time workers, people with inconsistent work histories and those already nearing retirement.

As discussions continue, Trump’s remarks have placed the issue firmly on the national agenda.

Whether the United States ultimately embraces elements of the Australian system will depend on political will, economic feasibility and how convincingly advocates can argue that compulsory savings would strengthen — rather than disrupt — the nation’s retirement landscape.

His remarks, highlighting what he described as a highly successful approach, have ignited a discussion over whether a similarly mandated structure could realistically function within the United States.

Australia’s superannuation framework requires employers to contribute a fixed portion of each employee’s wages into a managed retirement fund.

This locked-in savings mechanism has built one of the world’s largest national investment pools and provides most Australian workers with a reliable foundation for retirement income.

Trump praised the model for its discipline, stability and long-term performance, noting that it has produced stronger retirement outcomes than many voluntary savings systems.

The United States, by contrast, relies on a patchwork of employer-provided plans, personal savings and future Social Security benefits.

Millions of Americans lack access to retirement accounts, and savings levels vary widely across income groups.

Administration officials have indicated that exploring an Australian-style model reflects concerns about demographic pressures, widening savings gaps and growing uncertainty over the future strength of Social Security.

Supporters of the idea argue that a compulsory contribution system could dramatically strengthen the financial security of working Americans.

They point to Australia’s experience as evidence that consistent contributions and professional fund management build far more reliable retirement outcomes than voluntary systems, which often leave lower-income or irregular-income workers behind.

But major obstacles remain.

A mandate requiring employers to contribute to every worker’s retirement fund would mark a substantial shift from established U.S. labour and tax norms.

Small businesses, gig-economy employers and industries with fluctuating workforce patterns may find such requirements burdensome.

Transitioning the nation to a system resembling superannuation would also involve complex political negotiations and long-term legislative restructuring.

Some economists warn that, without additional safeguards, an imported model could deepen disparities among workers whose earnings patterns differ significantly from the more stable employment structures common in Australia.

They note that any American adaptation would need careful provisions to protect part-time workers, people with inconsistent work histories and those already nearing retirement.

As discussions continue, Trump’s remarks have placed the issue firmly on the national agenda.

Whether the United States ultimately embraces elements of the Australian system will depend on political will, economic feasibility and how convincingly advocates can argue that compulsory savings would strengthen — rather than disrupt — the nation’s retirement landscape.