Focus on the BIG picture.

Wednesday, May 13, 2026

Outside the box.

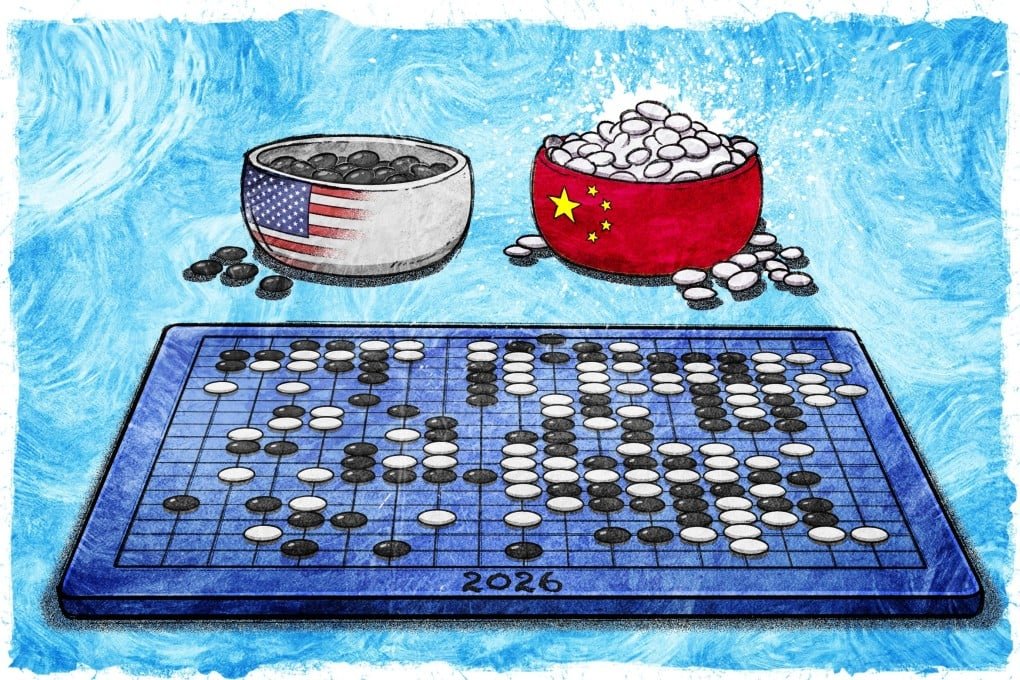

Trump Returns to a Hardened China as US–China Trade Rivalry Enters a New Phase

A new visit underscores how both economies have reshaped their trade exposure, with China reducing dependence on the US market while geopolitical shocks and energy pressures intensify global economic strain.

The global trade system underpinning US–China relations has evolved into a more fragmented and strategically insulated structure since the late 2010s, fundamentally changing the conditions surrounding high-level diplomatic visits between Washington and Beijing.

The dominant driver of this story is a system-level shift in global economic interdependence, where trade flows, industrial supply chains, and geopolitical risk are increasingly decoupled rather than tightly integrated.

The immediate context is the return of Donald Trump to China for the first time in nearly nine years, arriving into an environment shaped by intensified tariff regimes, expanded export controls on advanced technology, and accelerating supply chain diversification.

Compared with his earlier visit, when China was significantly more reliant on access to US consumer markets and technology inputs, the current landscape reflects a more balanced but more adversarial form of interdependence.

What is clearly established in the current phase of the US–China economic relationship is that both sides have actively reduced certain vulnerabilities.

China has expanded trade relationships across Southeast Asia, the Middle East, and parts of Latin America, while encouraging domestic substitution in strategic industries such as semiconductors, industrial equipment, and advanced manufacturing.

At the same time, multinational firms have increasingly shifted parts of their production networks to countries such as Vietnam and Indonesia to reduce exposure to concentrated risk.

The shift is visible at the firm level.

Export-oriented manufacturers that once depended heavily on US demand have adapted by diversifying production bases and customer markets.

This reduces immediate sensitivity to tariff shocks and trade policy uncertainty, even when US demand remains structurally important.

The result is a more distributed global manufacturing system in which no single bilateral relationship fully determines corporate survival.

The geopolitical environment surrounding the visit is also shaped by wider global instability, including disruptions in energy markets and heightened tensions in multiple regions.

These pressures have reinforced the strategic importance of securing resilient supply chains and diversified energy imports, further incentivizing countries to reduce overreliance on any single external partner.

China’s position entering this phase is structurally different from its position during earlier rounds of US trade pressure.

Its domestic industrial base is broader, its export destinations are more diversified, and its technological ecosystem has advanced in critical areas, even as it continues to face constraints in high-end semiconductor manufacturing and certain advanced computing inputs.

For the United States, the strategic challenge has also evolved.

Policy tools such as tariffs, export controls, and investment restrictions have reshaped supply chain geography, but they have not eliminated China’s central role in global manufacturing networks.

Instead, they have contributed to partial relocation of production and increased redundancy across multiple regions.

The result is not a clean decoupling but a restructuring of global economic connectivity.

Supply chains remain interconnected, but they are now routed through more countries, more regulatory frameworks, and more politically sensitive nodes.

This increases cost, complexity, and strategic uncertainty across industries ranging from consumer electronics to automotive manufacturing and energy-intensive production.

Against this backdrop, high-level visits carry symbolic weight beyond immediate policy outcomes.

They function as signals of how each side assesses the balance of leverage in a system where economic resilience has become as important as market access.

China’s expanded trade diversification and industrial depth give it greater negotiating stability than in earlier phases of the trade conflict, even as it remains exposed to external demand cycles.

The broader implication is that US–China relations have shifted from a phase of deepening integration to one of managed competition within a still-interconnected global economy.

The balance of power is no longer defined solely by access to markets, but by the ability to withstand disruption, reroute supply chains, and sustain industrial capacity under geopolitical pressure.

Trump’s arrival into this environment reflects not just a diplomatic moment, but the state of a global economic system that has been structurally reconfigured by nearly a decade of tariffs, technological restrictions, and strategic diversification across multiple continents.

The dominant driver of this story is a system-level shift in global economic interdependence, where trade flows, industrial supply chains, and geopolitical risk are increasingly decoupled rather than tightly integrated.

The immediate context is the return of Donald Trump to China for the first time in nearly nine years, arriving into an environment shaped by intensified tariff regimes, expanded export controls on advanced technology, and accelerating supply chain diversification.

Compared with his earlier visit, when China was significantly more reliant on access to US consumer markets and technology inputs, the current landscape reflects a more balanced but more adversarial form of interdependence.

What is clearly established in the current phase of the US–China economic relationship is that both sides have actively reduced certain vulnerabilities.

China has expanded trade relationships across Southeast Asia, the Middle East, and parts of Latin America, while encouraging domestic substitution in strategic industries such as semiconductors, industrial equipment, and advanced manufacturing.

At the same time, multinational firms have increasingly shifted parts of their production networks to countries such as Vietnam and Indonesia to reduce exposure to concentrated risk.

The shift is visible at the firm level.

Export-oriented manufacturers that once depended heavily on US demand have adapted by diversifying production bases and customer markets.

This reduces immediate sensitivity to tariff shocks and trade policy uncertainty, even when US demand remains structurally important.

The result is a more distributed global manufacturing system in which no single bilateral relationship fully determines corporate survival.

The geopolitical environment surrounding the visit is also shaped by wider global instability, including disruptions in energy markets and heightened tensions in multiple regions.

These pressures have reinforced the strategic importance of securing resilient supply chains and diversified energy imports, further incentivizing countries to reduce overreliance on any single external partner.

China’s position entering this phase is structurally different from its position during earlier rounds of US trade pressure.

Its domestic industrial base is broader, its export destinations are more diversified, and its technological ecosystem has advanced in critical areas, even as it continues to face constraints in high-end semiconductor manufacturing and certain advanced computing inputs.

For the United States, the strategic challenge has also evolved.

Policy tools such as tariffs, export controls, and investment restrictions have reshaped supply chain geography, but they have not eliminated China’s central role in global manufacturing networks.

Instead, they have contributed to partial relocation of production and increased redundancy across multiple regions.

The result is not a clean decoupling but a restructuring of global economic connectivity.

Supply chains remain interconnected, but they are now routed through more countries, more regulatory frameworks, and more politically sensitive nodes.

This increases cost, complexity, and strategic uncertainty across industries ranging from consumer electronics to automotive manufacturing and energy-intensive production.

Against this backdrop, high-level visits carry symbolic weight beyond immediate policy outcomes.

They function as signals of how each side assesses the balance of leverage in a system where economic resilience has become as important as market access.

China’s expanded trade diversification and industrial depth give it greater negotiating stability than in earlier phases of the trade conflict, even as it remains exposed to external demand cycles.

The broader implication is that US–China relations have shifted from a phase of deepening integration to one of managed competition within a still-interconnected global economy.

The balance of power is no longer defined solely by access to markets, but by the ability to withstand disruption, reroute supply chains, and sustain industrial capacity under geopolitical pressure.

Trump’s arrival into this environment reflects not just a diplomatic moment, but the state of a global economic system that has been structurally reconfigured by nearly a decade of tariffs, technological restrictions, and strategic diversification across multiple continents.