Focus on the BIG picture.

Saturday, May 16, 2026

Outside the box.

Trump’s Beijing Push Collides With Asia’s Fast-Moving Economic Realignment

As Donald Trump courts Chinese business ties alongside top US executives, a surge in Asian industrial investment is reshaping global economic power beyond Washington’s control.

System-driven changes in global capital allocation are redefining the relationship between the United States, China and the wider Asian economy, turning President Donald Trump’s latest Beijing visit into a negotiation shaped less by diplomacy alone than by a deeper industrial and financial transformation already underway.

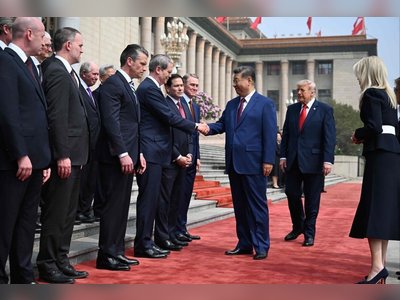

Trump arrived in Beijing this week accompanied by one of the largest and wealthiest American business delegations ever assembled for a presidential trip to China.

The executives represented industries spanning technology, finance, manufacturing, energy and infrastructure.

The visit focused heavily on restoring commercial momentum between the world’s two largest economies after years of tariffs, export controls, sanctions disputes and geopolitical confrontation.

But the broader economic backdrop has shifted substantially since Trump’s first presidency.

What is confirmed is that East Asia is now experiencing a sharp acceleration in capital expenditure tied to artificial intelligence infrastructure, advanced manufacturing, energy systems, defence production and supply-chain localization.

Investment banks, regional economists and corporate earnings data all point to a major industrial spending cycle spreading across China, South Korea, Japan, Taiwan, Singapore and parts of Southeast Asia.

The scale matters because it signals a redistribution of industrial gravity toward Asia at a moment when the United States is trying simultaneously to compete with China and maintain commercial access to Chinese markets.

The key issue is not whether American companies still want China’s business.

They clearly do.

The more important question is whether Asia’s economic system has become sufficiently self-reinforcing that Washington no longer occupies the same central position in regional growth that it once did.

Several forces are driving the shift simultaneously.

The global race to build artificial intelligence systems has created enormous demand for semiconductors, data centers, power infrastructure, industrial robotics and advanced cooling systems.

Regional governments and corporations are pouring money into those sectors at levels not seen since the industrial expansion cycle of the early two-thousands.

China occupies a uniquely powerful position in that ecosystem because of the depth of its manufacturing base.

The country produces critical components across nearly every industrial layer involved in modern infrastructure build-outs, including batteries, transformers, solar equipment, industrial machinery, consumer electronics and many semiconductor-linked materials.

That integration has allowed China to absorb external pressure more effectively than many Western policymakers expected during earlier phases of the US-China trade war.

Export controls and tariffs imposed by Washington accelerated some supply-chain diversification away from mainland China, particularly toward Vietnam, India and Mexico, but they also encouraged Beijing to intensify investment in domestic industrial capability.

The latest phase of geopolitical instability has added another layer.

The expanding conflict involving Iran and disruptions to Middle East energy routes have increased volatility in oil and shipping markets, pushing Asian governments to accelerate spending on energy security, renewables, electrification and strategic industrial resilience.

That trend benefits companies positioned around infrastructure and industrial production rather than purely consumer demand.

Across the region, corporations are increasing spending on factories, logistics systems, electricity grids and advanced computing capacity.

Trump’s visit therefore unfolded against a paradox.

American executives continue seeking access to Chinese consumers, manufacturing networks and financial markets even as Washington maintains strategic restrictions on advanced technology exports and tighter scrutiny of Chinese investment.

This tension defines the modern US-China economic relationship.

Rivalry and interdependence now operate simultaneously rather than separately.

The United States still attempts to constrain China’s technological rise in areas such as advanced semiconductors and military-linked artificial intelligence.

At the same time, major American corporations remain deeply exposed to Asian growth and cannot easily withdraw from the region without significant financial consequences.

The visit also highlighted a growing divide inside corporate America itself.

Some sectors continue advocating deeper engagement with China because of market scale and supply-chain efficiency.

Others increasingly support diversification due to geopolitical risk, sanctions exposure and uncertainty around future trade restrictions.

Financial markets across Asia have reacted accordingly.

Capital flows into infrastructure, AI-linked hardware, industrial automation and energy transition sectors have risen sharply over the past year.

Governments are competing to attract strategic manufacturing investment while simultaneously trying to reduce vulnerability to external shocks.

China’s leadership sees this environment as an opportunity rather than simply a challenge.

Beijing has spent years promoting industrial self-sufficiency, high-end manufacturing and domestic technological capability under broader national development strategies.

The current global environment — fragmented trade, geopolitical instability and competition over AI — reinforces those priorities.

At the same time, China still faces major structural economic pressures.

Property markets remain weak, local government debt burdens are high and consumer confidence has not fully recovered from years of economic slowdown.

Foreign investment into China has also become more selective due to regulatory concerns and geopolitical tensions.

Those weaknesses explain why Beijing still values engagement with US corporations despite escalating strategic rivalry.

Access to foreign capital, technology partnerships and international financial integration remains economically important even as China seeks greater independence from Western systems.

For the United States, the challenge is increasingly strategic rather than purely commercial.

Washington is attempting to slow China’s rise in critical technologies while preserving access to the very Asian growth engines driving global industrial expansion.

That balancing act becomes harder as regional economies deepen ties with one another independent of US influence.

Trade networks across East and Southeast Asia continue expanding, regional investment agreements are growing and Chinese supply chains remain embedded across much of the continent.

The result is a world economy becoming more regionally concentrated and less universally centered on the United States.

Trump’s Beijing visit demonstrated that American political and corporate leaders still view China as economically indispensable.

But it also exposed a more uncomfortable reality: Asia’s industrial transformation is now advancing under its own momentum, with or without Washington’s strategic approval.

The next phase of global competition will likely depend less on whether companies choose China or America and more on who controls the infrastructure, energy systems and industrial capacity powering the new AI-driven economy already taking shape across Asia.

Trump arrived in Beijing this week accompanied by one of the largest and wealthiest American business delegations ever assembled for a presidential trip to China.

The executives represented industries spanning technology, finance, manufacturing, energy and infrastructure.

The visit focused heavily on restoring commercial momentum between the world’s two largest economies after years of tariffs, export controls, sanctions disputes and geopolitical confrontation.

But the broader economic backdrop has shifted substantially since Trump’s first presidency.

What is confirmed is that East Asia is now experiencing a sharp acceleration in capital expenditure tied to artificial intelligence infrastructure, advanced manufacturing, energy systems, defence production and supply-chain localization.

Investment banks, regional economists and corporate earnings data all point to a major industrial spending cycle spreading across China, South Korea, Japan, Taiwan, Singapore and parts of Southeast Asia.

The scale matters because it signals a redistribution of industrial gravity toward Asia at a moment when the United States is trying simultaneously to compete with China and maintain commercial access to Chinese markets.

The key issue is not whether American companies still want China’s business.

They clearly do.

The more important question is whether Asia’s economic system has become sufficiently self-reinforcing that Washington no longer occupies the same central position in regional growth that it once did.

Several forces are driving the shift simultaneously.

The global race to build artificial intelligence systems has created enormous demand for semiconductors, data centers, power infrastructure, industrial robotics and advanced cooling systems.

Regional governments and corporations are pouring money into those sectors at levels not seen since the industrial expansion cycle of the early two-thousands.

China occupies a uniquely powerful position in that ecosystem because of the depth of its manufacturing base.

The country produces critical components across nearly every industrial layer involved in modern infrastructure build-outs, including batteries, transformers, solar equipment, industrial machinery, consumer electronics and many semiconductor-linked materials.

That integration has allowed China to absorb external pressure more effectively than many Western policymakers expected during earlier phases of the US-China trade war.

Export controls and tariffs imposed by Washington accelerated some supply-chain diversification away from mainland China, particularly toward Vietnam, India and Mexico, but they also encouraged Beijing to intensify investment in domestic industrial capability.

The latest phase of geopolitical instability has added another layer.

The expanding conflict involving Iran and disruptions to Middle East energy routes have increased volatility in oil and shipping markets, pushing Asian governments to accelerate spending on energy security, renewables, electrification and strategic industrial resilience.

That trend benefits companies positioned around infrastructure and industrial production rather than purely consumer demand.

Across the region, corporations are increasing spending on factories, logistics systems, electricity grids and advanced computing capacity.

Trump’s visit therefore unfolded against a paradox.

American executives continue seeking access to Chinese consumers, manufacturing networks and financial markets even as Washington maintains strategic restrictions on advanced technology exports and tighter scrutiny of Chinese investment.

This tension defines the modern US-China economic relationship.

Rivalry and interdependence now operate simultaneously rather than separately.

The United States still attempts to constrain China’s technological rise in areas such as advanced semiconductors and military-linked artificial intelligence.

At the same time, major American corporations remain deeply exposed to Asian growth and cannot easily withdraw from the region without significant financial consequences.

The visit also highlighted a growing divide inside corporate America itself.

Some sectors continue advocating deeper engagement with China because of market scale and supply-chain efficiency.

Others increasingly support diversification due to geopolitical risk, sanctions exposure and uncertainty around future trade restrictions.

Financial markets across Asia have reacted accordingly.

Capital flows into infrastructure, AI-linked hardware, industrial automation and energy transition sectors have risen sharply over the past year.

Governments are competing to attract strategic manufacturing investment while simultaneously trying to reduce vulnerability to external shocks.

China’s leadership sees this environment as an opportunity rather than simply a challenge.

Beijing has spent years promoting industrial self-sufficiency, high-end manufacturing and domestic technological capability under broader national development strategies.

The current global environment — fragmented trade, geopolitical instability and competition over AI — reinforces those priorities.

At the same time, China still faces major structural economic pressures.

Property markets remain weak, local government debt burdens are high and consumer confidence has not fully recovered from years of economic slowdown.

Foreign investment into China has also become more selective due to regulatory concerns and geopolitical tensions.

Those weaknesses explain why Beijing still values engagement with US corporations despite escalating strategic rivalry.

Access to foreign capital, technology partnerships and international financial integration remains economically important even as China seeks greater independence from Western systems.

For the United States, the challenge is increasingly strategic rather than purely commercial.

Washington is attempting to slow China’s rise in critical technologies while preserving access to the very Asian growth engines driving global industrial expansion.

That balancing act becomes harder as regional economies deepen ties with one another independent of US influence.

Trade networks across East and Southeast Asia continue expanding, regional investment agreements are growing and Chinese supply chains remain embedded across much of the continent.

The result is a world economy becoming more regionally concentrated and less universally centered on the United States.

Trump’s Beijing visit demonstrated that American political and corporate leaders still view China as economically indispensable.

But it also exposed a more uncomfortable reality: Asia’s industrial transformation is now advancing under its own momentum, with or without Washington’s strategic approval.

The next phase of global competition will likely depend less on whether companies choose China or America and more on who controls the infrastructure, energy systems and industrial capacity powering the new AI-driven economy already taking shape across Asia.