Focus on the BIG picture.

Thursday, Apr 03, 2025

Outside the box.

Potential Changes to Home Loan Regulations Could Increase Borrowing Power for Australian Buyers

If elected, the Coalition proposes reforms that may allow average borrowers to increase their home loan amounts significantly.

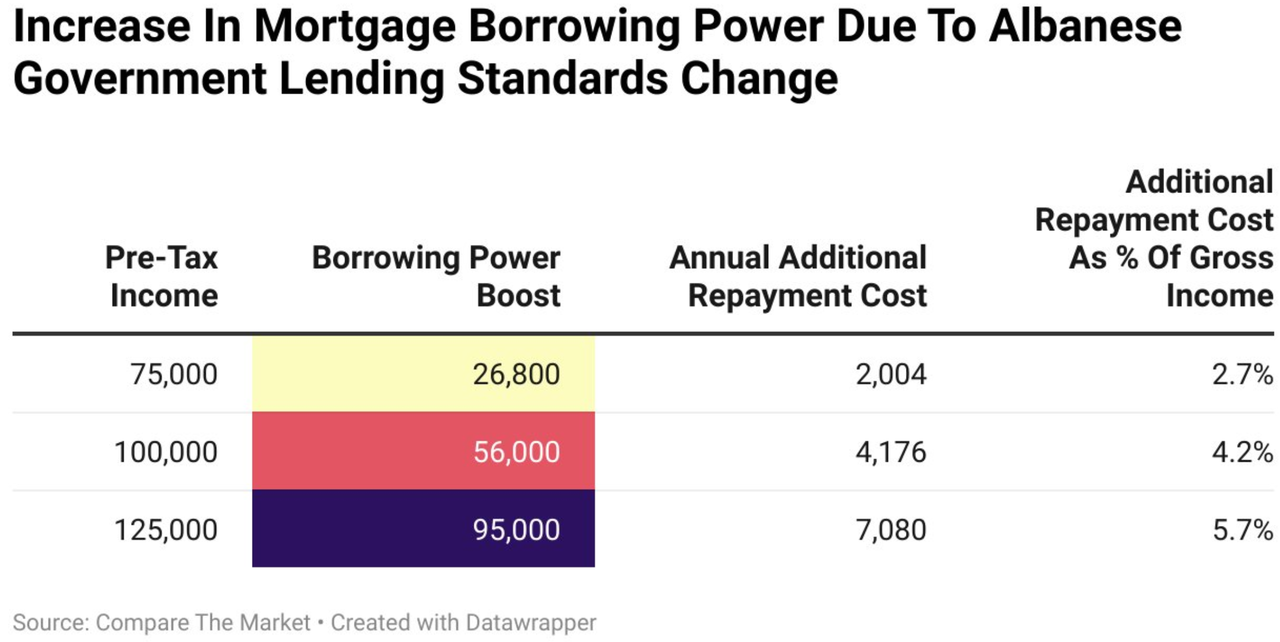

The Australian political landscape is poised for significant potential changes in housing finance as the Coalition, led by opposition housing spokesperson Michael Sukkar, outlines a plan that could enable average home buyers to borrow an additional $40,000.

The proposed reforms center on altering the policies set forth by the Australian Prudential Regulation Authority (APRA) regarding the serviceability buffer that banks must use to assess a borrower's ability to repay a loan amidst rising interest rates.

Currently, APRA mandates that financial institutions account for a 3 percent rise in interest rates when determining borrowing capacity.

This regulation was implemented during the COVID-19 pandemic, when the cash rate was recorded at a historic low of 0.1 percent.

Sukkar indicated that a reduction of this buffer could lead to increased borrowing power, specifically for first-time home buyers struggling to enter the housing market.

Financial analysis from Canstar suggests that a borrower with an average full-time salary of $103,024 could access an additional $40,000, should the buffer be decreased to 2 percent under a scenario of a 30-year loan at a 6 percent interest rate.

However, the exact extent to which the serviceability buffer would be modified remains uncertain, with Sukkar acknowledging that the final decision lies with APRA.

In addition to proposing changes to the serviceability buffer, the Coalition is also considering revisions to lenders mortgage insurance (LMI) requirements.

Currently, LMI is necessary for buyers who cannot provide a 20 percent deposit.

Sukkar contended that prospective buyers whose parents cannot support their loans should not face higher interest rates than others.

Experts have noted potential implications of altering the serviceability buffer.

Mardy Chiah, an associate professor of finance at the University of Newcastle, cautioned that while increasing borrowing capacities may assist buyers, it could paradoxically lead to inflated house prices driven by heightened demand.

The Property Council of Australia has supported these proposed reforms, with chief executive Mike Zorbas emphasizing the difficulties faced by first-home buyers in the current market.

He urged APRA to reconsider its regulations to promote home ownership while adapting to evolving market dynamics.

Responding to the Coalition's promises, Prime Minister Anthony Albanese raised concerns regarding clarity in the proposed changes.

He noted his government's initiatives aimed at facilitating housing opportunities for young Australians, which include policies to exclude Higher Education Contribution Scheme (HECS) debt from bank assessments for loans and introducing further discounts on educational debts.

Albanese also mentioned additional tax relief measures intended for young individuals entering the workforce and housing market.

As the federal election approaches, the implications of these proposed housing finance reforms continue to capture the attention of various stakeholders in Australia's housing sector.

The proposed reforms center on altering the policies set forth by the Australian Prudential Regulation Authority (APRA) regarding the serviceability buffer that banks must use to assess a borrower's ability to repay a loan amidst rising interest rates.

Currently, APRA mandates that financial institutions account for a 3 percent rise in interest rates when determining borrowing capacity.

This regulation was implemented during the COVID-19 pandemic, when the cash rate was recorded at a historic low of 0.1 percent.

Sukkar indicated that a reduction of this buffer could lead to increased borrowing power, specifically for first-time home buyers struggling to enter the housing market.

Financial analysis from Canstar suggests that a borrower with an average full-time salary of $103,024 could access an additional $40,000, should the buffer be decreased to 2 percent under a scenario of a 30-year loan at a 6 percent interest rate.

However, the exact extent to which the serviceability buffer would be modified remains uncertain, with Sukkar acknowledging that the final decision lies with APRA.

In addition to proposing changes to the serviceability buffer, the Coalition is also considering revisions to lenders mortgage insurance (LMI) requirements.

Currently, LMI is necessary for buyers who cannot provide a 20 percent deposit.

Sukkar contended that prospective buyers whose parents cannot support their loans should not face higher interest rates than others.

Experts have noted potential implications of altering the serviceability buffer.

Mardy Chiah, an associate professor of finance at the University of Newcastle, cautioned that while increasing borrowing capacities may assist buyers, it could paradoxically lead to inflated house prices driven by heightened demand.

The Property Council of Australia has supported these proposed reforms, with chief executive Mike Zorbas emphasizing the difficulties faced by first-home buyers in the current market.

He urged APRA to reconsider its regulations to promote home ownership while adapting to evolving market dynamics.

Responding to the Coalition's promises, Prime Minister Anthony Albanese raised concerns regarding clarity in the proposed changes.

He noted his government's initiatives aimed at facilitating housing opportunities for young Australians, which include policies to exclude Higher Education Contribution Scheme (HECS) debt from bank assessments for loans and introducing further discounts on educational debts.

Albanese also mentioned additional tax relief measures intended for young individuals entering the workforce and housing market.

As the federal election approaches, the implications of these proposed housing finance reforms continue to capture the attention of various stakeholders in Australia's housing sector.